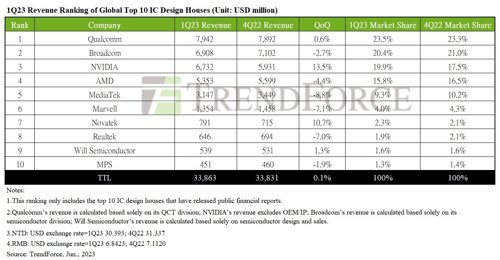

However, due to new product release and a surge in urgent orders for specialised specifications, Q1 revenue of the global top ten IC design houses remained on par with 4Q22, with a modest QoQ increase of 0.1% for a total revenue of $33.86 billion.

Changes in ranking included Cirrus Logic slipping from the top ten as well as the ninth and tenth positions being replaced by WillSemi and MPS, respectively. The rest of the rankings remained unchanged.

Qualcomm witnessed an uptick in its revenue, largely attributed to the launch and subsequent shipments of its latest flagship chip, the Snapdragon 8 Gen2. It saw a 6.1% in QoQ growth in its smartphone business, which effectively offset the downturn from its automotive and IoT sectors. As a result, Qualcomm’s Q1 revenue increased marginally by 0.6%, cementing its position as market leader with a 23.5% share.

Broadcom, however, is facing challenges stemming from the waning dividends of its product migration, coupled with a slowdown in demand for server storage and a seasonal downturn in the wireless sector. This led to a first-time quarterly decrease in revenue in 1Q23, with Broadcom’s revenue declining to $6.91 billion.

Nvidia experienced significant growth this quarter, fuelled by an explosive surge in demand for generative AI and cloud computing, alongside the introduction of the RTX 40 series. The company’s revenue from gaming and data centres saw a quarterly increase of 20% and 10%, respectively. This propelled Nvidia’s Q1 revenue by 13.5%, reaching $6.73 billion. Its market share is now close to 20%.

AMD struggled with inventory adjustments by some CSPs, weakened corporate expenditure due to macroeconomic influences, and a range of negative factors such as inventory modifications and an off-peak consumption period among PC-related clients.

Consequently, it saw a 21.8% and 18.2% QoQ decline in the revenue of its data centre and client divisions, respectively. Although there was growth in the embedded and gaming sectors, which helped counterbalance some of the downturn, AMD’s Q1 revenue still experienced a 4.4% reduction, falling to $5.35 billion.

MediaTek—during a lull in smartphone production and amid ongoing inventory adjustments in power management ICs—witnessed a 20% and 13% decline in its smartphone and power management IC sectors, respectively. Meanwhile, its business in smart edge platforms benefited from replenishment of TV-related inventory, ensuring the company’s revenue continued to remain on par with the previous quarter. Even though the extent of the quarterly decline was less severe than in the previous quarter, it was still greater than the company’s remaining top 5 competitors, dropping MediaTek’s market share from 10.2% last quarter to 9.3%. Consequently, MediaTek’s overall revenue in 1Q23 fell 8.8% to $3.15 billion.

Marvell’s Q1 revenue across all platforms was significantly impacted by adjustments in customer and channel inventories, leading to a QoQ decline of 7.1% and revenue falling to $1.35 billion. This dip occurred despite steady demand from servers, CSPs, and 5G-related wireless services.

When taking a look at variations in revenue across all platforms, both consumer products and data centres suffered a 10% decline. Seasonal factors were to blame for consumer products; for data centres, it was due to a slowdown in demand from on-premise enterprise businesses.

Novatek’s SoC and panel driver IC businesses experienced a QoQ growth of 24% and 2%, respectively, driven by the restocking of TV-related components. This led to a 10.7% increase in the company’s Q1 revenue, bringing it up to $791 million. Novatek maintained its seventh position with a market share of 2.3%.

Cirrus Logic, with over 80% of its revenue dependent on Apple alone, experienced a significant reduction in earnings due to factors such as a waning “new product” boost from the iPhone and a seasonal dip in sales.

Consequently, Cirrus Logic dropped out of the top ten.

The ninth and tenth positions have been filled by WillSemi and power management IC giant MPS. WillSemi reported a Q1 revenue of $539 million, marking a QoQ growth of 1.3%. MPS, however, witnessed a 1.9% QoQ decline, with its Q1 revenue standing at $451 million.

Looking ahead to the next quarter, although IC inventory clearance has been slower than anticipated, it has gradually rebounded to a healthier level in contrast to the period of excess inventory in 2H22. Simultaneously, the introduction of new products may stimulate positive growth for some IC design houses.

Nvidia, according to TrendForce, is one to watch. The rapid global deployment of AI chips—championed by CSPs and businesses and stimulated by the rising popularity of generative AI technologies like ChatGPT—is expected to trigger a swift revenue surge. Given these dynamics, it’s likely that Nvidia may rise to become the dominant IC design house in 2Q23.

This potential growth could not only boost Nvidia but also inspire a resurgence among the top ten global IC design houses, leading to a recovery from the market downturn.