That represents a 19.5% YoY decrease and a historic low in quarterly production since 2014 and suggests that a weakening global economy is impacting on consumer confidence.

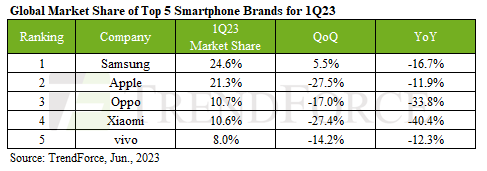

Looking more deeply at the figures Samsung saw a significant uptick in Q1 production thanks to the launch of its Galaxy S23 series, reaching 61.5 million units - a 5.5% QoQ rise. However, TrendForce is predicting a nearly 10% drop in Q2 production due to weakening demand for new models.

Apple faced a substantial 27.5% QoQ drop in smartphone production in Q1, delivering a total of 53.3 million units. The new iPhone 14 series accounted for approximately 78% of this figure, an improvement from the same period last year. Nonetheless, as the company navigates the transition period between model launches, a projected decrease of 20% is expected in Q2.

According to the report Oppo (which includes Oppo, Realme, and OnePlus) made strategic moves to reduce production in Q1 to 26.8 million units, a 17% QoQ decrease. However, TrendForce forecasts a more than 30% rise in Q2 production, attributed to successful inventory management and a moderate demand resurgence in Southeast Asia and other regions. Oppo has achieved notable sales success in South Asia, Southeast Asia, and Latin America. In fact, its overseas market accounts for nearly 60% of its total sales.

In the first quarter, Xiaomi (which includes Xiaomi, Redmi, POCO) saw its production volume dip to 26.5 million units, a 27.4% quarterly decrease. This decline was attributed to a global dip in consumer confidence and an overstocked inventory of finished products at Xiaomi, leading to restrained production plans. Due to ongoing inventory adjustments set for the second quarter, quarterly production growth is projected to be capped, with a modest estimated increase of around 20%.

Concurrently, Vivo (including Vivo, iQoo) reported a production volume of 20 million units for the first quarter, a 14.2% quarterly decrease. While China continues to be the primary market for Vivo's sales, Q2 demand continues to remain stagnant in the Chinese market, following the reopening of its borders. As a result, the quarterly production volume is anticipated to show a modest increase of around 10%.

The continuous economic slump has led to increased activity in the used phone and repair markets, which could potentially hinder Q2 smartphone production growth. Notwithstanding, Q2 production is forecasted to reach 260 million units, demonstrating a QoQ increase of around 5%. However, due to the unfavourable economic environment, TrendForce said that it expects smartphone production will fall by 10% when compared to the same period last year.