According to SEMI’s 300mm Fab Outlook Report to 2026, strong demand for high-performance computing, automotive applications and improved demand for memory will fuel double-digit spending in equipment investments over the three-year period.

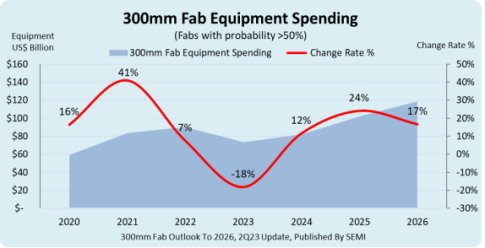

After the projected 18% drop to $74bn this year, global 300mm fab equipment spending is forecast to rise 12% to $82bn in 2024, 24% to $101.9bn in 2025 and 17% to $118.8bn in 2026.

“The projected equipment spending growth wave underscores the strong secular demand for semiconductors,” said Ajit Manocha, SEMI President and CEO. “The foundry and memory sectors will figure prominently in this expansion, pointing to demand for chips across a wide breadth of end markets and applications.”

Korea is expected to lead global 300mm fab equipment spending in 2026 with $30.2bn in investments, nearly doubling from $15.7bn this year. Taiwan is forecast to invest $23.8bn in 2026, up from US$22.4bn this year, while China is projected to see $16.1bn in spending in 2026, an increase from $14.9bn in 2023.

America’s equipment spending is expected to nearly double from $9.6bn this year to $18.8bn in 2026.

Foundry is projected to lead other segments in equipment spending at $62.1bn in 2026, an increase from $44.6bn in 2023, followed by memory at $42.9bn, a 170% increase from 2023. Analogue spending is forecast to increase from $5bn this year to $6.2bn in 2026. The microprocessor/microcontroller, discrete (mainly power devices), and optoelectronics segments are expected to see spending declines in 2026, while investments in logic is forecast to rise.

The SEMI 300mm Fab Outlook Report To 2026 report lists 369 facilities and lines globally, including 53 high-probability facilities expected to start operation during the four years starting in 2023.